FATCA Compliance for U.S. Expats in Paraguay: 2026 Guide

FATCA compliance for U.S. expats in Paraguay requires timely filing of IRS Form 8938 and FinCEN Form 114 (FBAR) when foreign financial assets exceed defined thresholds. Both filings are separate obligations. Ignoring either one exposes you to penalties that start at $10,000 and can climb far higher. Paraguay's territorial tax system makes it an attractive base for American remote workers, but it does not reduce or replace your U.S. reporting duties. This guide covers every threshold, deadline, and filing step you need to stay fully compliant in 2026.

What are the FATCA and FBAR reporting thresholds for expats in Paraguay?

FATCA compliance for expats in Paraguay centers on two distinct forms with different thresholds. Knowing exactly which one applies to your situation prevents both over-filing and costly missed filings.

Form 8938 thresholds for U.S. expats abroad

Hands holding FATCA Form 8938 threshold sheet

Form 8938 thresholds for Americans living outside the United States are higher than for those living stateside. The IRS sets them as follows:

| Filing status | Year-end value | Any time during the year |

|---|

| Single / Married Filing Separately | $200,000 | $300,000 |

| Married Filing Jointly | $400,000 | $600,000 |

The "any time during the year" column is the one that catches most expats off guard. A single large transfer in march that later drops below $200,000 by december can still trigger a filing requirement.

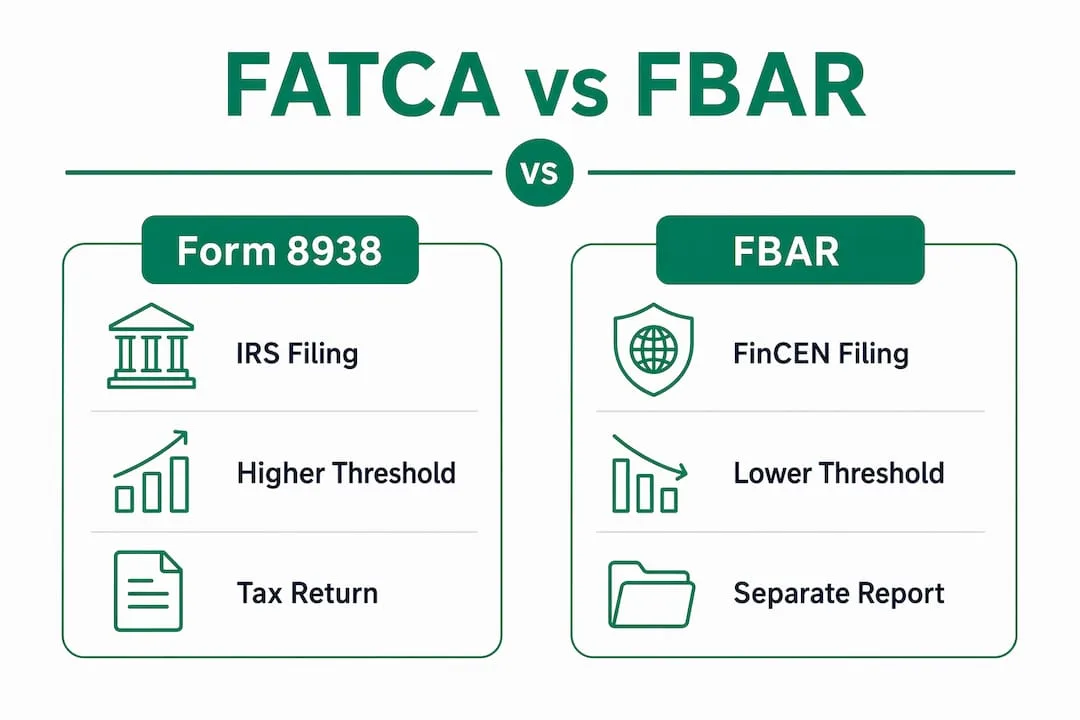

FBAR thresholds and key differences

Infographic comparing FATCA and FBAR requirements

FBAR filing is required when the aggregate maximum value of all your foreign financial accounts exceeds $10,000 at any point during the calendar year. That threshold is far lower than Form 8938, and it applies to the combined total across all accounts, not each account individually.

Key differences between the two filings:

- Form 8938 is filed with the IRS and attached to your federal tax return (Form 1040).

- FBAR (FinCEN Form 114) is filed separately with the Financial Crimes Enforcement Network (FinCEN), not the IRS.

- Form 8938 covers a broader range of foreign financial assets, including certain foreign stock and securities.

- FBAR covers foreign bank and financial accounts only.

- Both can apply simultaneously to the same accounts.

Pro Tip: You may owe both filings for the same accounts. Meeting the FBAR threshold does not exempt you from Form 8938, and vice versa.

How do you file Form 8938 and FBAR as a U.S. expat in Paraguay?

Filing correctly requires following a specific process for each form. The two systems are entirely separate, and mixing up their procedures is one of the most common compliance errors.

-

Gather your account records. Collect statements from every Paraguayan and foreign bank account, brokerage, and financial institution you hold. Note the highest balance each account reached at any point during the year, not just the year-end figure.

-

Complete Form 8938. Form 8938 must be attached to your IRS Form 1040. You cannot file it as a standalone document. If you file a tax return extension, Form 8938 follows the same extended deadline.

-

File your FBAR electronically. FBAR is filed through the FinCEN BSA E-Filing system at bsaefiling.fincen.treas.gov. It is completely separate from your IRS tax return. The standard deadline is april 15, with an automatic extension to october 15 for U.S. persons abroad.

-

Document peak balances. Monthly account snapshots are the most reliable way to capture the highest balance during the year. Relying on year-end statements alone can cause you to miss a filing trigger.

-

Submit and retain records. Keep copies of both filings and all supporting account statements for at least six years. The IRS statute of limitations for FATCA-related issues can extend well beyond the standard three years.

Pro Tip: If you extend your tax return to october 15, your Form 8938 extension follows automatically. Your FBAR also extends to october 15, but that extension is automatic and does not require a separate request.

Consequences for late or missed filings are severe. A missed Form 8938 triggers a $10,000 penalty immediately. After 90 days of continued noncompliance following an IRS notice, the penalty increases by $10,000 for every additional 30-day period, up to $50,000 more. That means total exposure of up to $60,000 for a single missed filing year.

What penalties do U.S. expats in Paraguay face for FATCA and FBAR violations?

Penalty exposure for FATCA and FBAR noncompliance is one of the most serious financial risks U.S. expats face. The amounts are not proportional to the size of your accounts.

Form 8938 penalty schedule:

- Initial failure-to-file penalty: $10,000

- Continued noncompliance after IRS notice: additional $10,000 per 30-day period

- Maximum additional penalty: $50,000

- Total maximum exposure per year: $60,000

FBAR penalty structure:

- Non-willful violations: up to $10,000 per violation

- Willful FBAR violations: up to $100,000 or 50% of the account balance, whichever is greater

The willful vs. non-willful distinction matters enormously. Many expats assume "willful" means intentional fraud. It does not.

"Recklessness satisfies the willfulness standard for FBAR penalties." — Second Circuit Court of Appeals, 2026

This ruling means that reckless disregard of your filing obligations, such as ignoring known requirements or failing to check whether you qualify, can expose you to the highest penalty tier. You do not need to have intended to break the law.

Practical challenges that increase penalty risk for Paraguay-based expats include:

Need personalized help?

Get expert guidance for your Paraguay relocation journey. Our team is here to help you with residency, business setup, real estate, and banking solutions.

- Tracking account balances monthly across multiple Paraguayan banks

- Misunderstanding how tax return extensions interact with Form 8938 deadlines

- Assuming Paraguay's Common Reporting Standard (CRS) participation replaces U.S. FATCA obligations. It does not. CRS and FATCA are parallel systems. Paraguay's CRS reporting to foreign governments has no effect on your personal IRS filing requirements.

How does Paraguay tax residency affect your FATCA obligations?

Paraguay tax residency and U.S. tax obligations operate on completely separate legal tracks. Understanding both is critical for expats managing compliance on two fronts.

Paraguay tax residency requirements

Paraguay tax residency is established by spending 120 or more days in the country during a fiscal year, or by having your center of vital interests (primary home, family, business) in Paraguay. Once established, you receive a tax residency certificate, which Paraguayan banks and government entities use to confirm your local tax status.

Paraguay taxes only income sourced within Paraguay. Foreign-source income, including remote work income paid by U.S. clients, is generally taxed at 0% under Paraguay's territorial tax system. That is a significant advantage for American remote workers.

How the two systems compare

| Factor | Paraguay tax system | U.S. tax system |

|---|

| Tax basis | Territorial (Paraguay-source only) | Worldwide income |

| Residency trigger | 120+ days or center of vital interests | U.S. citizenship / Green Card |

| Foreign income tax | 0% | Taxable (credits may apply) |

| FATCA / FBAR filing | Not applicable | Required when thresholds are met |

U.S. citizens remain subject to worldwide income taxation regardless of where they live. Obtaining a Paraguay residency certificate satisfies local bank and government requirements, and it can support your case for certain IRS foreign tax credits or exclusions. It does not, however, eliminate your Form 8938 or FBAR obligations.

Pro Tip: Present your Paraguay tax residency certificate to local banks proactively. It clarifies your tax status under both CRS and local regulations, and it reduces the chance of account reporting complications.

FATCA regulations in Paraguay are also mediated through intergovernmental agreements (IGAs) between the U.S. and partner jurisdictions. Under these agreements, Paraguayan financial institutions may register with the IRS and report U.S. account holders. That institutional reporting does not replace your personal filing obligation. You must still file Form 8938 and FBAR independently when thresholds are met.

Key Takeaways

U.S. expats in Paraguay must file both Form 8938 and FBAR independently when thresholds are met, regardless of Paraguay's territorial tax system or local CRS reporting.

| Point | Details |

|---|

| Two separate filings required | Form 8938 goes to the IRS with your tax return; FBAR goes to FinCEN electronically. |

| FBAR threshold is very low | Any time your combined foreign accounts exceed $10,000, FBAR filing is required. |

| Recklessness equals willfulness | Ignoring known FBAR obligations can trigger penalties up to $100,000 or 50% of account balance. |

| Paraguay residency does not cancel U.S. duties | A Paraguay tax certificate helps locally but does not reduce IRS reporting requirements. |

| Track peak balances monthly | Year-end statements alone can cause you to miss a filing trigger for both forms. |

What I've learned watching expats get this wrong

Most compliance problems I see among U.S. expats in Paraguay are not caused by bad intentions. They are caused by two specific misunderstandings that are completely avoidable.

The first is the CRS confusion. Expats hear that Paraguay participates in the Common Reporting Standard and assume their local bank is already reporting everything to the IRS on their behalf. That is not how it works. CRS reports go to other governments, not directly to the IRS in a way that satisfies your personal filing obligation. You still need to file Form 8938 and FBAR yourself.

The second is the peak balance problem. Most people check their account balance in december and use that number. If your account hit $320,000 in july and dropped to $180,000 by year-end, you still triggered the Form 8938 "any time during the year" threshold as a single filer. Catching that requires monthly tracking, not annual reviews.

My strong recommendation is to work with a tax professional who specializes in U.S./Paraguay cross-border tax law, not a general CPA who handles expat returns as a side service. The nuances around Form 8938 attachment timing, FBAR standalone deadlines, and the recklessness standard for willful penalties are specific enough that generalist advice creates real risk. Start your compliance review early in the calendar year, before balances shift and deadlines approach.

— Alejandro

How Movetoparaguay supports your tax compliance in Paraguay

Navigating U.S. tax obligations from Paraguay is manageable with the right support structure in place. Movetoparaguay works directly with U.S. expats and remote workers to address both sides of the compliance picture: Paraguayan tax residency certification and U.S. reporting requirements.

The team at Movetoparaguay provides personalized consultations that review your specific financial situation, residency status, and filing history before recommending next steps. Services include assistance with Paraguay tax residency documentation, company formation, and ongoing compliance support. Every case is reviewed individually, so you receive guidance that fits your actual circumstances rather than generic advice. Visit Movetoparaguay to learn how the team can help you stay compliant on both fronts.

FAQ

What is FATCA and does it apply to U.S. expats in Paraguay?

FATCA (Foreign Account Tax Compliance Act) requires U.S. citizens to report foreign financial assets above set thresholds to the IRS using Form 8938. It applies to all U.S. citizens abroad, including those living in Paraguay.

What is the FBAR threshold for expats in Paraguay?

FBAR filing is required when the combined maximum value of all foreign financial accounts exceeds $10,000 at any point during the calendar year. This threshold applies to the aggregate across all accounts, not each account separately.

Does Paraguay tax residency eliminate U.S. FATCA obligations?

No. Paraguay tax residency satisfies local banking and government requirements, but U.S. citizens remain subject to worldwide income reporting and must still file Form 8938 and FBAR when thresholds are met.

What is the penalty for missing a Form 8938 filing?

The initial penalty is $10,000. After 90 days of continued noncompliance following an IRS notice, an additional $10,000 per 30-day period applies, up to a maximum of $50,000 more, for a total potential penalty of $60,000 per year.

Can recklessness trigger the highest FBAR penalties?

Yes. The Second Circuit Court of Appeals confirmed in 2026 that reckless disregard of FBAR obligations satisfies the willfulness standard, exposing expats to penalties up to $100,000 or 50% of the account balance.