Bona Fide Residence Test for U.S. Expats: 2026 Guide

The bona fide residence test is defined by the IRS as a qualification standard that determines whether a U.S. taxpayer has established genuine, uninterrupted residence in a foreign country for at least one full tax year. Passing this test unlocks access to the Foreign Earned Income Exclusion (FEIE), governed by Internal Revenue Code Section 911, which allows eligible taxpayers to exclude up to $130,000 of foreign earned income from U.S. taxation in 2025. Both U.S. citizens and qualifying resident aliens can use this test. Understanding what is bona fide residence test means understanding that it is not simply about counting days abroad. The IRS evaluates the full picture of your life, including your intent, your ties to a foreign country, and how deeply you have integrated into life there.

What are the criteria for the bona fide residence test?

The IRS requires uninterrupted residence abroad for a complete calendar tax year, meaning january 1 through december 31, to qualify under this test. That is the hard floor. You cannot start the clock in march and count it as a qualifying year. Your residence must span the entire year without a break that signals you have abandoned your foreign home.

Beyond the calendar year requirement, the IRS evaluates a set of qualitative factors to determine whether your residence is genuine. These factors include:

- Intent to remain indefinitely. You must not have a fixed return date to the U.S. A temporary assignment with a planned end date disqualifies you.

- Tax home in a foreign country. Your regular place of business or employment must be located abroad, not in the United States.

- Family and household relocation. Moving your spouse and children abroad strengthens your case significantly.

- Social and economic integration. Joining local organizations, opening foreign bank accounts, and paying local taxes all signal genuine residence.

- Visa status. Holding a long-term visa or permanent residency permit in the host country supports your claim.

- Severing U.S. ties. Selling your U.S. home, canceling U.S. club memberships, or transferring financial accounts abroad reinforces your intent.

The IRS evaluates intent and integration as primary factors, not just physical presence. That distinction matters enormously when your file lands on an auditor's desk.

You are also permitted to take brief trips back to the U.S. during your qualifying period. Temporary U.S. visits do not break your bona fide residence status, provided you maintain a clear intent to return to your foreign home. Vacations, family emergencies, and short business trips are all acceptable.

Expat couple discussing bona fide residence criteria at café

Expat couple discussing bona fide residence criteria at caféOne important exception applies when you are forced to leave a country due to war, civil unrest, or similar dangerous conditions. The IRS publishes a list of qualifying countries each year in the Internal Revenue Bulletin where this waiver applies. If you were evacuated from a qualifying country, you may still meet the test even without completing the full calendar year.

Pro Tip: Start your foreign residency on january 1 if at all possible. Moving abroad mid-year means you cannot qualify under the bona fide residence test until december 31 of the following year, adding a full extra year to your waiting period.

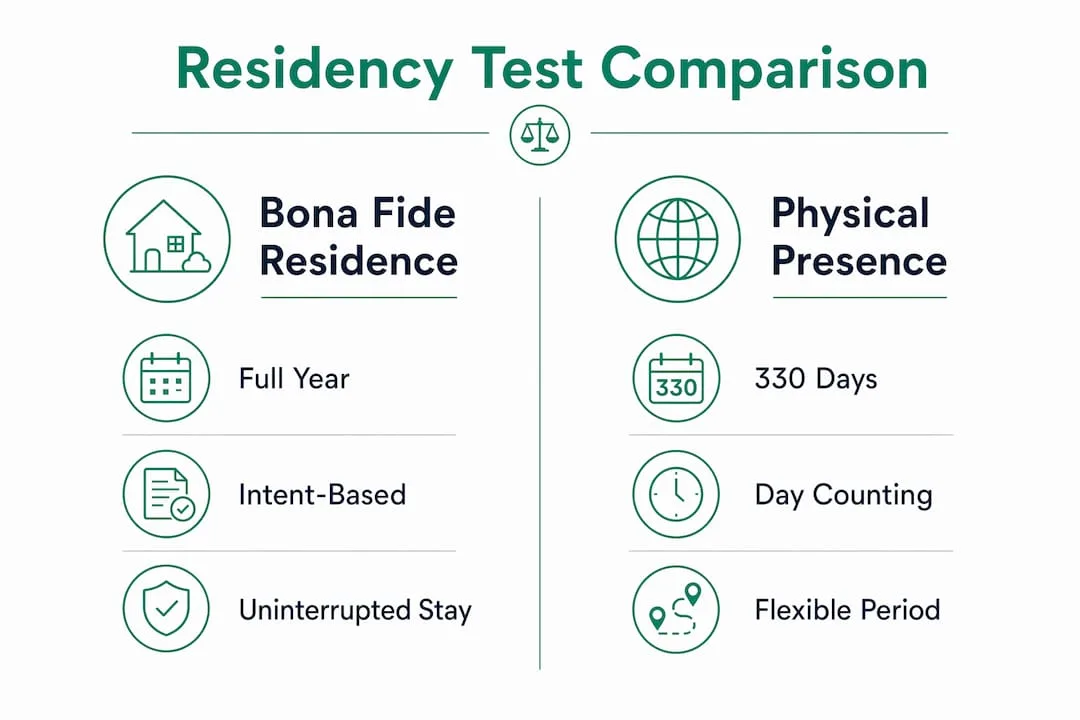

How does the bona fide residence test compare with the physical presence test?

The IRS offers two separate tests for qualifying for the FEIE. Understanding the difference between them helps you choose the right path for your situation.

Infographic comparing bona fide residence and physical presence tests

Infographic comparing bona fide residence and physical presence testsThe physical presence test requires 330 full days of presence in foreign countries during any 12-month period. It is a math problem. You count days, and if you hit 330, you qualify. The bona fide residence test, by contrast, asks the IRS to evaluate your life circumstances, your intent, and your integration into a foreign country. One test is objective; the other is subjective.

| Criteria | Bona fide residence test | Physical presence test |

|---|

| Qualifying standard | Genuine residence for a full calendar year | 330 full days in any 12-month period |

| IRS evaluation method | Qualitative, intent-based | Quantitative, day-count-based |

| Flexibility on timing | Must cover jan 1 to dec 31 | Any rolling 12-month period |

| Audit risk | Higher due to subjectivity | Lower due to objective counting |

| Resident alien eligibility | Requires tax treaty in some cases | No treaty requirement |

| Best suited for | Long-term expats with deep local ties | Frequent travelers and first-year expats |

The physical presence test suits expats who travel frequently between countries or who moved abroad partway through a year. The bona fide residence test suits expats who have fully relocated their lives and can demonstrate deep integration in one country.

Tax professionals recommend using the physical presence test when your calendar year timeline is ambiguous, because it removes the subjectivity that can trigger IRS scrutiny. If you can qualify under both tests, the physical presence test is often the safer filing choice for your first year abroad.

Pro Tip: You can switch between tests from year to year. If your first year abroad is a partial year, use the physical presence test. Once you have completed a full calendar year abroad, evaluate whether the bona fide residence test better fits your situation.

What documentation proves bona fide residence to the IRS?

Building a strong paper trail is the most practical thing you can do to protect your FEIE claim. The IRS does not pre-approve bona fide residence status. You self-declare on Form 2555, and the IRS evaluates your claim after the fact, often during an audit. Your documentation is your defense.

Follow these steps to build a solid record:

- Secure a long-term housing lease or property deed abroad. A signed lease in your name, showing your foreign address, is one of the strongest pieces of evidence you can hold.

- Enroll your children in local schools. School enrollment records demonstrate that your family has genuinely relocated, not just extended a vacation.

- Open a local bank account and transfer your primary financial activity. Foreign bank statements showing regular deposits and local bill payments show economic integration.

- Pay local taxes and comply with host country requirements. Foreign tax receipts or tax filings in your host country confirm you are participating in the local system, not just passing through.

- Keep a detailed travel log. Record every entry and exit date for both the U.S. and your host country. Include the purpose of each trip. This log becomes critical if the IRS questions your uninterrupted residence.

- File Form 2555 correctly and completely. This form requires you to state your foreign address, the date your bona fide residence began, and the country where you reside. Errors or omissions invite follow-up questions.

- Gather supporting documents proactively. Utility bills, gym memberships, local club registrations, and community organization records all add texture to your claim.

The IRS looks for the center of gravity of your life. The more of your life that is anchored abroad, the stronger your position.

What are the common IRS scrutiny risks with the bona fide residence test?

The bona fide residence test carries more audit risk than the physical presence test because the IRS makes a judgment call, not a calculation. Several specific situations increase that risk.

- Moving abroad after january 1. If you relocate in april, you cannot qualify for that tax year under the bona fide residence test. Trying to force qualification in a partial year is a common and costly mistake. The physical presence test is the correct tool for that situation.

- Retaining significant U.S. ties. Keeping a U.S. home, maintaining voter registration in a U.S. state, or holding a U.S. driver's license as your primary ID all signal that your center of gravity remains in the United States.

- Returning to the U.S. frequently for extended periods. Brief trips are acceptable, but long stays that look like you are living in the U.S. part-time undermine your claim.

- Holding a temporary work visa abroad. A tourist visa or short-term work permit suggests you do not intend to remain indefinitely. Long-term residency permits carry far more weight.

- Resident alien status without a qualifying tax treaty. Resident aliens must often meet treaty requirements to use the bona fide residence test, unlike U.S. citizens who face no such restriction.

- Failing to document intent. The IRS evaluates intent through evidence, not statements. Saying you intended to stay indefinitely means nothing without documentation to support it.

Need personalized help?

Get expert guidance for your Paraguay relocation journey. Our team is here to help you with residency, business setup, real estate, and banking solutions.

If your situation involves any of these risk factors, consult a qualified tax professional before filing Form 2555. The cost of professional advice is far lower than the cost of an IRS dispute over a disallowed FEIE claim. For expats facing an active dispute, IRS audit reconsideration is a formal process worth understanding.

Key Takeaways

The bona fide residence test requires genuine, uninterrupted foreign residence for a full calendar year, evaluated by the IRS through qualitative factors including intent, integration, and documentation.

| Point | Details |

|---|

| Full calendar year required | Residence must cover january 1 through december 31 with no qualifying break. |

| Intent outweighs day counts | The IRS prioritizes your intent to remain and your economic integration over physical presence alone. |

| Form 2555 is self-declared | The IRS does not pre-approve status; your documentation must be audit-ready from day one. |

| Physical presence test is safer for partial years | If you moved abroad mid-year, use the physical presence test to avoid disqualification. |

| Documentation is your defense | Leases, foreign tax records, school enrollment, and travel logs form the core of a strong FEIE claim. |

What I have learned from watching expats navigate this test

The most common mistake I see is treating the bona fide residence test like a checklist. Expats move abroad, rent an apartment, open a bank account, and assume they are covered. The IRS does not see it that way. What the IRS actually looks for is whether your life has genuinely moved. That means your family, your finances, your social connections, and your long-term plans all point to the foreign country, not back to the U.S.

The second mistake is timing. Expats who move in july and try to claim bona fide residence for that year are setting themselves up for a disallowed exclusion. The calendar year rule is absolute. There is no workaround, and attempting one creates a paper trail that looks worse than simply using the physical presence test for the first year.

What actually works is early planning and honest self-assessment. If your ties to the U.S. are still strong, the bona fide residence test may not be the right tool yet. Give yourself time to genuinely relocate your life before claiming the exclusion under this standard. The FEIE is worth protecting. A disallowed claim, with penalties and back taxes, can erase years of tax savings in one audit cycle.

— Alejandro

How Movetoparaguay supports U.S. expats with tax residency planning

U.S. expats who want to establish genuine foreign residency and qualify for the FEIE need more than general advice. They need a structured plan built around their specific circumstances.

Movetoparaguay provides tailored residency consultations for U.S. expats, covering everything from legal residency permits to ongoing tax compliance in Paraguay. Paraguay's territorial tax system generally applies 0% tax on foreign-source income, making it one of the most practical destinations for expats seeking to reduce their global tax burden. Movetoparaguay's team reviews your individual situation, explains your next steps clearly, and supports you through the documentation process that makes a bona fide residence claim defensible. Learn more about U.S. expat tax residency services and how Paraguay fits your financial goals.

FAQ

What is the bona fide residence test in simple terms?

The bona fide residence test is an IRS standard that determines whether a U.S. taxpayer has established genuine residence in a foreign country for a full calendar year. Passing it qualifies you to claim the Foreign Earned Income Exclusion on Form 2555.

How long do you have to live abroad to pass the bona fide residence test?

You must be a bona fide resident of a foreign country for an uninterrupted full tax year, meaning january 1 through december 31. Partial years do not qualify under this test.

Can you travel back to the U.S. and still pass the bona fide residence test?

Yes. Brief and temporary trips to the U.S. do not break your bona fide residence status, as long as you maintain a clear intent to return to your foreign home. Extended stays that suggest you are living in the U.S. part-time create audit risk.

What is the difference between the bona fide residence test and the physical presence test?

The physical presence test requires 330 full days abroad in any 12-month period and is based on day counting. The bona fide residence test is qualitative and evaluates your intent, integration, and ties to a foreign country over a full calendar year.

Does the IRS approve bona fide residence status before you file?

No. The IRS does not pre-approve bona fide residence status. You self-declare on Form 2555, and the IRS evaluates your claim based on your documentation, which may be reviewed during an audit.