Dual Tax Residency Issues Resolved: A Clear Guide

Dual tax residency is defined as the legal condition in which two countries simultaneously claim you as a tax resident under their domestic laws. This situation is common for mobile professionals, U.S. expats, and remote workers who split time across borders. The good news: dual tax residency issues resolved through a structured sequence of treaty tie-breaker rules under Article 4(2) of the OECD Model Tax Convention, which most bilateral treaties adopt. Understanding this process is the first step toward compliance, not panic.

How do domestic laws create dual residency conflicts?

Dual residency begins at the domestic law level, before any treaty applies. Each country sets its own rules for who qualifies as a tax resident, and those rules frequently overlap for people who live internationally.

Common domestic residency triggers include:

- Physical presence tests: Many countries use a 183-day threshold. Spend more than 183 days in a country during a tax year, and that country claims you as a resident.

- Permanent home availability: Some jurisdictions, including the United Kingdom and Germany, treat you as a resident if you maintain a home there, regardless of how many days you actually spend in it.

- Domicile and intent: The United States taxes its citizens on worldwide income regardless of where they live, creating an automatic overlap with any foreign residency.

- Registration and social ties: Countries like France and Spain consider registration with local authorities, family location, and economic ties as residency indicators.

Relying solely on day counts is one of the most common mistakes people make. Many audits fail precisely because individuals assumed residency was determined by days spent in a country, when domestic law actually weighs permanent home availability and personal ties far more heavily.

Dual residency under domestic law is a legally valid and common condition for globally mobile individuals. Treaties exist to allocate taxing rights between the two countries, but they do not automatically erase your domestic filing obligations in either jurisdiction. Understanding this distinction protects you from assuming treaty relief does more than it actually does. For a deeper look at how residency status affects your obligations, the Movetoparaguay guide on tax resident vs. nonresident is a practical starting point.

Man reviewing tax residency documents at desk

Man reviewing tax residency documents at deskWhat is the sequence of treaty tie-breaker rules?

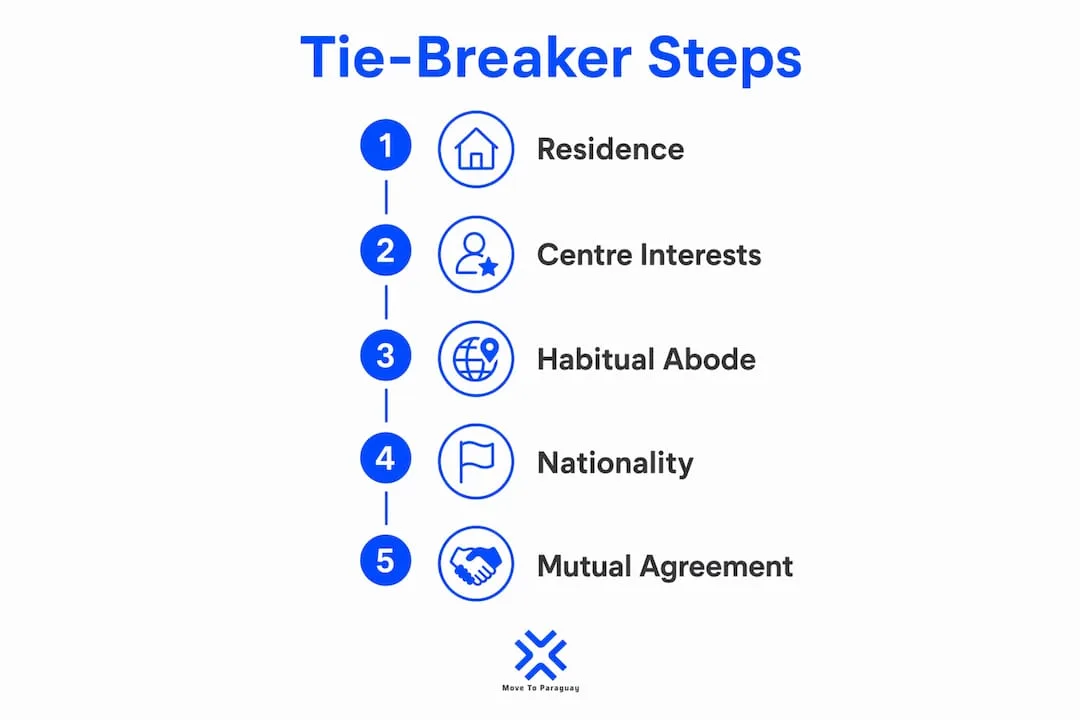

The OECD Model Tax Convention provides a five-step hierarchy to resolve dual tax residency conflicts. Analysis stops the moment one step produces a clear result. You do not need to work through all five steps if an earlier one settles the question.

-

Permanent home availability. The first question is whether you have a permanent home available to you in one or both countries. "Available" means a home you can use at any time, not just one you own. If you have a permanent home in only one country, that country wins the tie-breaker at this step.

-

Centre of vital interests. If you have permanent homes in both countries, the analysis shifts to where your personal and economic life is centered. The centre of vital interests test weighs family location, primary employment, main bank accounts, doctors, clubs, and social ties. Personal ties carry special weight when economic ties are split between two countries. A person whose spouse and children live in Portugal, but whose employer is based in the United Kingdom, would likely have their centre of vital interests in Portugal.

-

Habitual abode. When the centre of vital interests cannot be determined, the tie-breaker moves to where you habitually reside. This is not simply a day count. It examines the regularity, frequency, and pattern of your stays in each country over a defined period.

-

Nationality. If habitual abode is also inconclusive, the treaty assigns residence to the country of which you are a national. For dual nationals, this step also fails to resolve the conflict, and the analysis moves to the final step.

-

Mutual Agreement Procedure (MAP). When none of the first four steps produces a clear result, the tax authorities of both countries negotiate directly to assign treaty residence. MAP is a formal government-to-government process and can take considerable time to conclude.

Pro Tip: Document your position at each step, even if you resolve the conflict at Step 1 or Step 2. Tax authorities in both countries may audit your treaty claim years later, and a written record of your analysis at the time of filing is far more defensible than a reconstructed argument.

The five-step hierarchy in Article 4(2) of the OECD Model Tax Convention is adopted by the majority of bilateral treaties, including the U.S.-U.K., U.S.-Portugal, and Canada-Spain agreements. Knowing which treaty applies to your specific situation determines exactly which version of these rules governs your case.

Infographic outlining OECD treaty tie-breaker steps

Infographic outlining OECD treaty tie-breaker stepsWhat documentation do you need to claim treaty-based relief?

Claiming treaty relief requires more than knowing which country wins the tie-breaker. You need a paper trail that proves your position to both tax authorities.

Core documents to maintain:

- Certificate of residence: Issued by the tax authority of your treaty-residence country. This is the primary document used to claim treaty benefits abroad.

- Lease or property ownership records: Prove where your permanent home is located and when it was available to you.

- Travel logs and passport stamps: Support your habitual abode and physical presence claims with dated evidence.

- Employment contracts and pay stubs: Establish where your economic activity is centered.

- Bank and financial account records: Demonstrate where your primary financial ties are held.

- Family registration documents: School enrollment, medical records, and utility bills in your name all support centre of vital interests claims.

Required forms by jurisdiction:

| Jurisdiction | Required Form | Purpose |

|---|

| United States | IRS Form 1040-NR + Form 8833 | Disclose treaty-based return position |

| United Kingdom | Self-assessment return + certificate of residence | Claim treaty relief and prove residency |

| European Union (varies) | Local tax return + residence certificate | Substantiate treaty residence in each member state |

Filing IRS Form 8833 is mandated by the Internal Revenue Code whenever a taxpayer takes a treaty-based position that overrides or modifies U.S. tax law. Skipping this form is a compliance failure, even if your underlying treaty claim is correct.

Dual tax residency resolution is an annual, fact-dependent process. Changes in employment, housing, or duration of stay can alter your tie-breaker outcome from one year to the next. Tax professionals advise a yearly review to prevent liability surprises and maintain eligibility for treaty relief. The Movetoparaguay resource on the bona fide residence test explains the documentation standards the IRS applies when evaluating primary residency claims.

Pro Tip: Keep a single organized folder, updated annually, that contains your certificate of residence, travel log, lease or property records, and the prior year's filed returns. If you are ever audited in either country, this folder is your first line of defense.

Consistent factual narratives aligned with treaty language across multiple years strengthen your position and reduce audit risk. Tax professionals advise maintaining stable, treaty-based positions tied to dated documents and evidence. Changing your story from year to year is the fastest way to attract scrutiny from both tax authorities simultaneously.

Need personalized help?

Get expert guidance for your Paraguay relocation journey. Our team is here to help you with residency, business setup, real estate, and banking solutions.

What happens when tie-breaker rules don't resolve the conflict?

Some dual residency situations resist resolution through the standard five-step hierarchy. When that happens, the Mutual Agreement Procedure becomes the path forward.

Key facts about MAP:

- MAP is a government-to-government process. You cannot participate directly. Your role is to submit a formal request to the competent authority of one or both treaty countries, presenting your facts and asking them to negotiate on your behalf.

- Resolution takes time. Average MAP resolution exceeds 24 months. Filing conflicting returns in both countries while MAP is pending increases your audit exposure and complicates the negotiation.

- Early professional involvement matters. Early professional counsel is critical when MAP appears necessary. A tax professional who understands both jurisdictions can present a unified, coherent narrative to both competent authorities, which improves cooperation and speeds resolution.

- Suspend aggressive positions during MAP. Avoid taking contradictory treaty positions in your annual filings while the procedure is active. Conflicting filings between jurisdictions prolong disputes and increase audit risks.

- Document your MAP request thoroughly. Include a full chronology of your residency facts, copies of all relevant documents, and a clear explanation of why the standard tie-breaker steps did not produce a definitive result.

If your situation involves New York State tax obligations alongside a federal dual residency conflict, specialized New York tax relief services can help you manage both the state and federal dimensions simultaneously.

Key Takeaways

Dual tax residency issues are resolved by applying the OECD five-step tie-breaker hierarchy, maintaining consistent annual documentation, and invoking MAP only when the standard rules fail to produce a clear result.

| Point | Details |

|---|

| Domestic law creates the conflict | Two countries can legally claim you as a resident simultaneously before any treaty applies. |

| Five-step hierarchy assigns treaty residence | The OECD tie-breaker sequence stops at the first step that produces a clear result. |

| Documentation is your defense | Certificates of residence, travel logs, and Form 8833 are required to substantiate treaty claims. |

| Annual reassessment is mandatory | Changes in housing, employment, or travel patterns can shift your tie-breaker outcome each year. |

| MAP resolves what tie-breakers cannot | Government-to-government negotiation is the formal path when the standard hierarchy fails. |

What I've learned from watching people get dual residency wrong

Most people I work with arrive believing dual residency is a crisis. It is not. Dual residence is a normal legal condition for globally mobile taxpayers. The crisis comes from mismanaging it, not from the status itself.

The single most damaging mistake I see is inconsistency across years. Someone claims their centre of vital interests is in Paraguay in year one, then files as a U.S. resident in year two without updating their treaty position. Both tax authorities notice. Both start asking questions. What could have been a clean, defensible position becomes a multi-year dispute.

The second mistake is treating treaty relief as a one-time fix. Your residency facts change. Your housing changes. Your family situation changes. A treaty position that was airtight in 2024 may be weak in 2026 if you have not updated your documentation to reflect your current circumstances. Annual review is not optional. It is the difference between a defensible position and an expensive audit.

My honest advice: build your treaty position like you are building a legal record, because you are. Date every document. Keep every lease. Log every trip. Write a short annual memo to your own file explaining why your treaty-residence conclusion is the same or different from the prior year. That memo, written at the time of filing, is worth more than any argument you reconstruct three years later under audit pressure.

— Alejandro

How Movetoparaguay helps you resolve dual residency challenges

Dual residency conflicts require jurisdiction-specific knowledge and consistent execution across multiple tax years. Movetoparaguay specializes in exactly this kind of structured, long-term residency planning for U.S. expats and remote workers.

Movetoparaguay provides tailored consultations that review your individual residency facts in detail, identify your treaty tie-breaker position, and map out the specific next steps for your situation. Services include Paraguayan company formation, ongoing tax compliance, and documentation support to substantiate your residency claims across jurisdictions. Paraguay's territorial tax system generally applies 0% tax on foreign-source income, making it a practical and legally sound base for resolving dual residency conflicts. If you are ready to get your residency position on solid ground, explore your options with Movetoparaguay today.

FAQ

What does dual tax residency mean?

Dual tax residency means two countries simultaneously claim you as a tax resident under their domestic laws. Treaties resolve the conflict by assigning treaty residence to one country through a structured tie-breaker hierarchy.

Does dual residency always mean double taxation?

No. Tax treaties allocate taxing rights between the two countries, preventing the same income from being fully taxed twice. However, treaty residence does not eliminate all domestic filing obligations in either jurisdiction.

What is the centre of vital interests test?

The centre of vital interests test identifies where your personal and economic life is most concentrated, weighing factors like family location, primary employment, and main bank accounts. It applies when you have a permanent home available in both treaty countries.

How long does Mutual Agreement Procedure take?

MAP resolution typically exceeds 24 months. Early professional involvement and a unified, well-documented presentation to both competent authorities improve the speed and outcome of the negotiation.

Do I need to file Form 8833 to claim treaty benefits in the U.S.?

Yes. The Internal Revenue Code requires Form 8833 whenever a taxpayer takes a treaty-based position that overrides or modifies U.S. tax law. Filing without it is a compliance failure regardless of whether your underlying treaty claim is correct.