Tax Resident vs. Nonresident: What Expats Must Know

Tax residency status is defined by whether the IRS taxes you on your worldwide income or only on certain U.S.-source income. That single distinction shapes every tax form you file, every deduction you can claim, and every penalty you risk. The difference between tax resident and nonresident status is not a technicality. It is the foundation of your entire U.S. tax obligation. The IRS determines your status through two formal tests: the Green Card Test and the Substantial Presence Test. Getting this wrong costs real money.

What tests determine the difference between tax resident and nonresident?

The IRS uses two official tests to classify you as a resident alien or a nonresident alien for tax purposes. Passing either one makes you a tax resident for that year.

The Green Card Test

The Green Card Test is straightforward. If you held lawful permanent resident status at any point during the calendar year, you are a U.S. tax resident for that entire year. This applies even if you spent most of the year outside the United States. The test does not measure days. It measures legal immigration status.

Hands arranging green card and tax documents

Hands arranging green card and tax documentsThe Substantial Presence Test

The Substantial Presence Test uses a weighted three-year day count formula. To pass the test and become a tax resident, you must meet two conditions:

- Be present in the U.S. for at least 31 days during the current year.

- Reach a total of 183 days using this weighted formula:

- Count all days present in the current year.

- Count one-third of days present in the prior year.

- Count one-sixth of days present in the year before that.

Here is a concrete example: you spend 120 days in the U.S. in each of the past three years. Your calculation is 120 (current year) + 40 (one-third of 120) + 20 (one-sixth of 120) = 180 days. That total falls below the 183-day threshold, so you remain a nonresident alien for tax purposes. One more day in the current year would push you over.

The closer connection exception

Passing the Substantial Presence Test does not automatically lock in resident status. Taxpayers who meet the day count but maintain a closer connection to a foreign country can file for a nonresident exception. The IRS looks at where your permanent home is, where your family lives, and where your economic ties are strongest. This exception requires filing IRS Form 8840 and documenting your ties clearly.

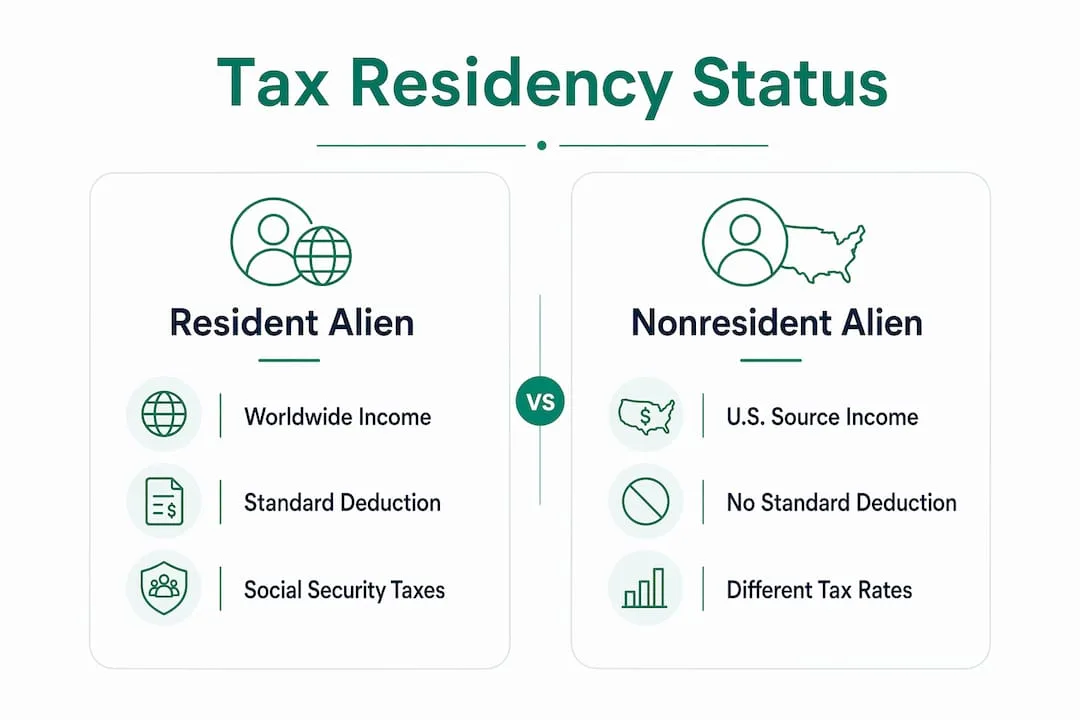

Infographic comparing tax resident and nonresident aliens

Infographic comparing tax resident and nonresident aliensPro Tip: Track your U.S. entry and exit dates in a dedicated calendar or spreadsheet every year. Customs and Border Protection records arrivals, but not always departures. Your own records are your best defense in a residency dispute.

How does tax residency status affect your U.S. tax obligations?

The tax implications of nonresident status versus resident status are significant. They affect which forms you file, which income you report, and which deductions you can take.

Income reporting differences

- Resident aliens report all worldwide income on Form 1040, the same form U.S. citizens use. This includes wages, investment income, rental income, and business profits earned anywhere in the world.

- Nonresident aliens report only U.S.-source income and income effectively connected to a U.S. trade or business on Form 1040-NR. Foreign-source income is generally excluded entirely.

- Nonresident aliens cannot claim the standard deduction. They may only itemize deductions directly connected to their effectively connected income.

Tax rates applied to nonresidents

Nonresident aliens face two distinct tax rate structures. Effectively Connected Income (ECI) is taxed at the same graduated rates that apply to residents. Fixed, Determinable, Annual, or Periodical income (FDAP), which includes dividends, interest, and royalties, is taxed at a flat 30% rate unless a tax treaty reduces it.

| Income Type | Resident Alien | Nonresident Alien |

|---|

| Worldwide income | Fully taxable | Not taxable |

| U.S.-source income (ECI) | Graduated rates | Graduated rates |

| FDAP income | Graduated rates | 30% flat (or treaty rate) |

| Standard deduction | Available | Not available |

| Form filed | Form 1040 | Form 1040-NR |

Social Security and Medicare taxes

Resident aliens pay Social Security and Medicare taxes on U.S. wages, just like citizens. Most nonresident aliens also pay these taxes on U.S. wages, but specific visa categories such as F-1 and J-1 student visas carry exemptions. Confirming your visa category and its tax treatment is a separate step from determining residency status.

What happens if you have dual status or residency conflicts?

Dual status occurs when your residency classification changes during a single calendar year. This is common for expats who arrive in the U.S. mid-year and meet the Substantial Presence Test, or who give up a green card partway through the year.

In a dual-status year, you file two separate returns or a combined return that separates income earned as a nonresident from income earned as a resident. The rules are strict. You cannot use the standard deduction for the resident portion if you were a nonresident for any part of the year.

International residency conflicts add another layer. Two countries can each claim you as a tax resident under their own domestic laws. This is where Double Taxation Agreements (DTAs) become critical. A DTA is a treaty between two countries that prevents the same income from being taxed twice.

- Permanent home: The treaty first asks where you have a permanent home available to you.

- Center of vital interests: If you have a permanent home in both countries, the treaty looks at where your personal and economic ties are stronger.

- Habitual abode: If the center of vital interests cannot be determined, the treaty checks where you spend more time habitually.

- Nationality: As a final tie-breaker, some treaties use citizenship.

DTAs resolve which country gets primary taxing rights, but they do not eliminate domestic filing requirements in both countries. You may still need to file returns in both jurisdictions, even if you owe tax only in one.

Pro Tip: If a DTA applies to your situation, file IRS Form 8833 to disclose your treaty position. Failing to file this form can result in penalties even when the treaty itself reduces your tax bill to zero.

What are common mistakes in determining tax residency?

Misclassifying your residency status is one of the most common tax filing mistakes expats make. The consequences range from overpaying taxes to facing penalties for underreporting income.

Here are the most frequent errors and how to avoid them:

-

Treating the 183-day rule as automatic. Many expats assume that spending fewer than 183 days in the U.S. guarantees nonresident status. The weighted three-year formula means your prior two years of presence also count. You can trigger residency with far fewer than 183 days in the current year if your prior years were heavy.

-

Filing the wrong form. Filing Form 1040 when you should file Form 1040-NR, or vice versa, creates mismatches in income reporting and deduction eligibility. Misclassifying tax residency leads to erroneous tax calculations that the IRS will catch.

Need personalized help?

Get expert guidance for your Paraguay relocation journey. Our team is here to help you with residency, business setup, real estate, and banking solutions.

-

Ignoring the closer connection exception. Expats who pass the Substantial Presence Test but have strong ties to another country often miss the Form 8840 filing. This exception can legally preserve nonresident status and significantly reduce your U.S. tax exposure.

-

Overlooking treaty provisions. Many countries have DTAs with the United States that modify standard residency rules. Relying solely on domestic IRS tests without checking applicable treaty language is a costly oversight.

-

Poor day-tracking documentation. The IRS can request proof of your physical presence. Passport stamps, boarding passes, hotel receipts, and credit card records all serve as evidence. Reconstruct your travel history annually, not years later when records are harder to find.

"Tax residency experts emphasize early verification of status to avoid compliance errors and penalties from incorrect filing." Verify your residency classification before you file, not after a notice arrives.

The 183-day rule is also not universally decisive across countries. Many jurisdictions weigh family ties, housing, and economic connections alongside day counts. If you split time between multiple countries, each country's domestic rules and any applicable DTA must be reviewed independently.

Key takeaways

Tax residency status is the single most consequential classification in cross-border tax compliance, and getting it right requires applying the correct IRS tests, tracking your days accurately, and checking applicable tax treaties before you file.

| Point | Details |

|---|

| Two tests determine U.S. residency | The Green Card Test and Substantial Presence Test are the only IRS-recognized methods for classifying resident vs. nonresident status. |

| Income scope differs sharply | Residents report worldwide income on Form 1040; nonresidents report only U.S.-source income on Form 1040-NR. |

| The 183-day rule is not automatic | The weighted three-year formula means prior years of U.S. presence count toward the threshold, not just the current year. |

| Treaties resolve dual residency | Double Taxation Agreements use a cascade of tie-breaker tests, but filing obligations in both countries may still apply. |

| Early verification prevents penalties | Confirming your residency status before filing avoids misclassification errors that trigger IRS penalties or overpayments. |

Why I tell every expat to verify residency status before anything else

I have worked with expats who spent years filing the wrong return. Not because they were careless. Because the rules genuinely look simpler than they are. The Substantial Presence Test sounds like a day-counting exercise until you realize your 2023 and 2024 travel history is already baked into your 2025 calculation.

The closer connection exception is the most underused tool I see. Expats who clearly live abroad, own property abroad, and have their families abroad still file as residents because they hit the day count and assumed that settled it. It does not. The IRS gives you a legal path to nonresident status if your ties to another country are stronger. Most people never take it because they do not know it exists.

Dual-status years are where I see the most expensive mistakes. A mid-year move triggers a filing structure that most tax software handles poorly. The income allocation between your resident and nonresident periods must be exact. Getting it wrong means either overpaying or underreporting, and neither outcome is good.

My consistent advice: assess your residency status in january of each year, not in april when you are rushing to file. Pull your travel records, count your days using the weighted formula, check whether a DTA applies, and then decide which form you are filing. That sequence takes an hour. Fixing a misclassification after the fact takes months. You can also watch a short expat tax overview to get oriented before diving into the details.

— Alejandro

How Movetoparaguay supports expats with tax residency clarity

Movetoparaguay works specifically with U.S. expats and remote workers who need to get their tax residency right, not just in the U.S., but in their new country of residence. Paraguay operates on a territorial tax system, which generally means 0% tax on foreign-source income. That structure makes residency classification especially valuable for expats earning income outside Paraguay.

Movetoparaguay offers tailored consultations that review your individual situation in detail, including your U.S. filing obligations, your Paraguayan residency status, and how the two interact. Services include company formation, ongoing tax compliance support, and clear guidance on timelines and fees. If you are ready to understand exactly where you stand, Movetoparaguay is the place to start.

FAQ

What is the main difference between a tax resident and a nonresident?

A tax resident is taxed on worldwide income, while a nonresident is taxed only on U.S.-source or effectively connected income. The IRS determines this status through the Green Card Test and the Substantial Presence Test.

How do I calculate days under the Substantial Presence Test?

Count all days in the current year, add one-third of days from the prior year, and add one-sixth of days from the year before that. If the total reaches 183 and you were present at least 31 days this year, you meet the test.

Can I be a nonresident even if I pass the 183-day count?

Yes. If you pass the Substantial Presence Test but have a closer connection to a foreign country, you can file IRS Form 8840 to claim nonresident status. You must document your ties to the foreign country clearly.

What form does a nonresident alien file with the IRS?

Nonresident aliens file Form 1040-NR to report U.S.-source income. They cannot claim the standard deduction and may only deduct expenses directly connected to their effectively connected income.

Do tax treaties eliminate the need to file in both countries?

No. A Double Taxation Agreement resolves which country has primary taxing rights, but it does not remove domestic filing requirements. You may still need to file returns in both countries even if you owe tax in only one.